President Trump signed the Tax Cuts and Jobs Act (P.L. 115-97) (The Act) into law on December 22, 2017. The Act provides the most sweeping change to the U.S. tax code since 1986. This historic bill calls for lowering the individual and corporate tax rates, repealing countless tax credits and deductions, enhancing the child tax credit, boosting business expensing and more. The final law varies from the first version passed by the House, and the second version as adjusted and passed by the Senate. Congress passed the final version after a joint conference committee made numerous adjustments to the bill. The bill passed 227-203 in the House and 51-47 in the Senate; with 12 Republicans voting against it and no Democrats voting for it.

The new tax laws are incorporated into the 2018.1 release of Sage Fixed Assets─Depreciation. See our January 25, 2018 blog post for more details on this release.

This post covers the most common, but not all, provisions in the Act affecting depreciation and expense deductions for the U.S. taxation of business property (generally, fixed assets used in business).

At a Glance

- 100% bonus expensing for qualifying property, starting 9/28/2017

- Section 179 expensing increased to $1,000,000 per year, starting 2018

- Yearly automobile depreciation caps almost tripled, starting 2018

- AMT for corporations is repealed, starting 2018

Why would a taxpayer use Section 179 expensing if 100% bonus is allowed?

Bonus must be applied to all qualifying property, unless elected out. Election out can be made by classes of property (i.e. 5-year, 7-year). Section 179 can be selectively applied to individual assets. A company’s over-all tax situation will determine if one or the other, or a mix of the two, is best.

In Depth

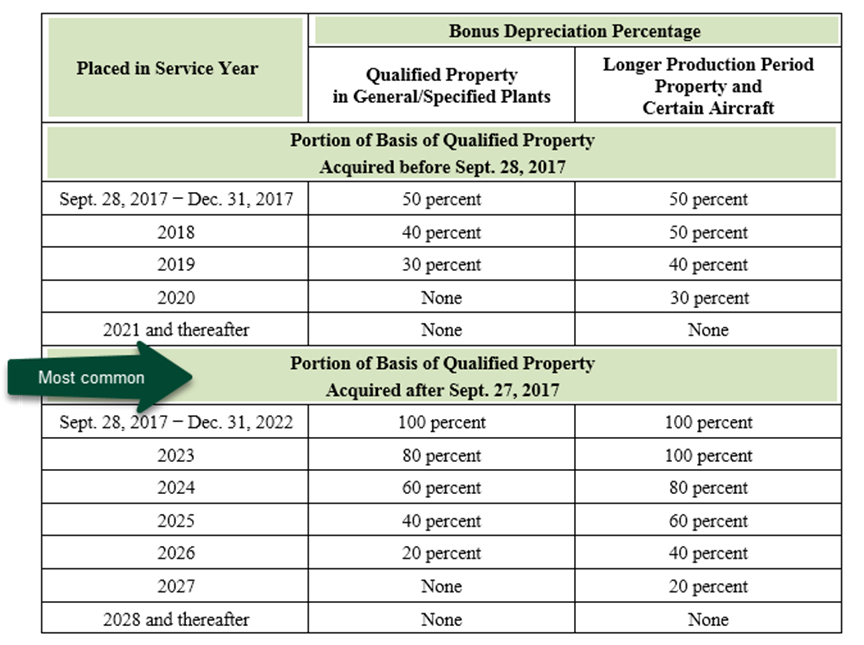

Bonus Depreciation (Section 168(k) Allowance)

In general, for qualified property acquired after 9/27/2017 and placed in service by 12/31/2022, the 50% bonus rate is increased to 100%, and then phased-out over the following years.

- Used property qualifies for bonus, if it meets certain acquisition requirements.

- Qualified improvement property qualifies for bonus, assuming the below technical correction is made (see Recovery Period for Real Property).

- The first-year passenger vehicle caps continue to be increased by $8,000, in most cases, when bonus is taken.

- The Act retains the current step-down in rates (50%, 40%, 30%) for property acquired BEFORE 9/28/2017, and placed in service in later periods.

- Taxpayers can elect 50%, instead of the new 100% rate, for property acquired and placed in service from 9/28/2017 to the end of their first taxable year ending after 9/27/2017.

The applicable rates, by acquisition date of the property, are:

Section 179 Expensing

The Act expands expensing under Section 179 for business property placed in service in taxable years beginning on or after 1/1/2018 as follows:

- Increases the limit to $1,000,000

- The 2017 limit remains $510,000

- Increases the phase-out threshold to $2,500,000

- The 2017 threshold remains $2,030,000

- The new limit and threshold will be adjusted for inflation beginning in 2019 taxable years

- The $25,000 cap on SUVs will also be adjusted for inflation beginning in 2019

- Changes definition of “qualified real property” to:

- any qualified improvement property described in section 168(e)(6) and any of the following improvements to non-residential real property:

- Roofs

- Heating, ventilation, and air-conditioning property

- Fire protection and alarm systems

- Security systems

- any qualified improvement property described in section 168(e)(6) and any of the following improvements to non-residential real property:

- The exclusion from expensing for property used in connecting with lodging facilities, such as residential rental property, is eliminated.

Recovery Period for Real Property

Effective for property placed in service 1/1/2018 and later:

- Eliminated the 15-year qualified leasehold, retail, and restaurant improvement property classes

- Assigned a 15-year recovery period to qualified improvement property, assuming a technical correction is made.

- The original Senate bill provided a 10-year recovery period, the House bill did not have the 10-year provision. The text of the final bill does not have the provision for a 15-year life, however, according to the Conference Report on H.R. 1, the act sets a 15-year recovery period for qualified improvement property. Therefore, a technical correction is expected.

- Qualified improvement property is depreciated using the straight-line method and half-year convention or, if applicable, the mid-quarter convention

Depreciation caps on passenger automobiles

The annual depreciation caps, that apply to many cars, trucks and vans, are increased for vehicles placed in service after December 31, 2017.

The increased caps for vehicles placed in service in 2018 are:

Tax Year 1...............$10,000 ($18,000 if bonus depreciation claimed)

Tax Year 2...............$16,000

Tax Year 3...............$9,600

Tax Years 4 + ..........$5,760

- The bonus increase is lower if 50%, 40% or 30% bonus is required. A lower rate is required if the vehicle is acquired pre-9/28/2017 (see Bonus Percentage table above).

- The caps will be indexed for inflation after 2018.

AMT for Corporations Repealed

The Alternative Minimum Tax (AMT) is repealed for corporations for tax filing years 2018 and thereafter. This will reduce tax compliance work for accountants that handle a corporation's AMT and ACE (Adjusted Current Earnings) depreciation calculations. Previously, only "small business corporations" were exempt from the AMT rules. However, if their 3-year average gross receipts exceeded a certain level, they lost the exemption. Now all corporations are exempt under the new law. The AMT rules are still in effect for individuals.

Depreciation of Farm Property

The following applies to new farming machinery and equipment placed in service after December 31, 2017:

- A decrease in the 7-year recovery period for new farming machinery and equipment to 5 years, and

- Elimination of the rule requiring use of the 150-percent-declining balance method on property used in a farming business (thus 200% DB can be used)

- ADS (alternative depreciation system) required if farming business elects out of interest deduction limits.

Like-kind Exchanges of Property

Effective for disposals/exchanges after 2017 (with some exceptions):

- Like-kind exchange treatment is no longer allowed for depreciable tangible personal property, and intangible and non-depreciable personal property.

- Like-kind exchanges are limited to real property. Thus, as under current law, no gain or loss is recognized on the exchange of real property held for productive use in a trade or business or for investment if that real property is exchanged solely for real property of like kind that will be held either for productive use in a trade or business or for investment.